The difference between Malaysia and Indonesia payroll systems is something most foreign companies get wrong when they cross the border and run their first payroll in the new country.

A German manufacturing company expanded from Kuala Lumpur to Jakarta after three successful years in Malaysia. Their regional HR director was confident. The team understood statutory contributions, had clean EPF and SOCSO records, and ran payroll without issues. Indonesia felt like a natural next step: same region, similar business cultures, familiar enough.

The first Jakarta payroll run produced three compliance errors simultaneously. BPJS Ketenagakerjaan was configured as a single program when it’s actually five. The annual THR religious holiday allowance, which has no Malaysian equivalent, wasn’t budgeted. And PPh 21 was being calculated using an annualisation method that Indonesia replaced with the TER system in January 2024.

None of these were negligence. They were the consequence of assuming that two neighbouring countries with similar GDP trajectories and overlapping business cultures had built their workforce compliance systems on similar logic. They hadn’t.

Two Countries, One Dangerous Assumption

The Malaysia vs Indonesia payroll comparison starts with a philosophical difference that shapes everything downstream.

Malaysia’s payroll system is relatively unified. Three major statutory contributions are administered through two government bodies, with standardised rates and a single monthly deadline:

- EPF (Employee Provident Fund) for retirement savings

- SOCSO (Social Security Organisation) for workplace injury, occupational disease, and invalidity protection

- EIS (Employment Insurance System) for job loss protection

PCB income tax withholding follows tables published by LHDN. The system is complex enough to require careful administration, but its architecture is consistent across industries and regions.

Indonesia’s payroll system is structurally more fragmented. BPJS operates two separate agencies, BPJS Kesehatan for health and BPJS Ketenagakerjaan for employment, with different contribution structures, different wage caps, and different payment deadlines.

PPh 21 income tax calculation was overhauled in January 2024 and now uses a three-category effective rate system that most global payroll tools haven’t fully accommodated.

Regional minimum wages vary significantly by province, for example, Jakarta’s minimum wage differs from Surabaya’s or Yogyakarta’s. And Indonesia has a mandatory allowance that Malaysia does not: THR (the religious holiday bonus).

For foreign companies operating across both markets, the dangerous assumption is that payroll knowledge transfers. It doesn’t, not cleanly. The terminology overlaps enough to create false confidence, and the actual mechanisms diverge enough to create costly compliance gaps.

The structural difference between Malaysia and Indonesia payroll systems becomes obvious only when companies attempt to run payroll across both markets using the same assumptions.

Also read: HR Risks in Foreign Company Expansion to Indonesia

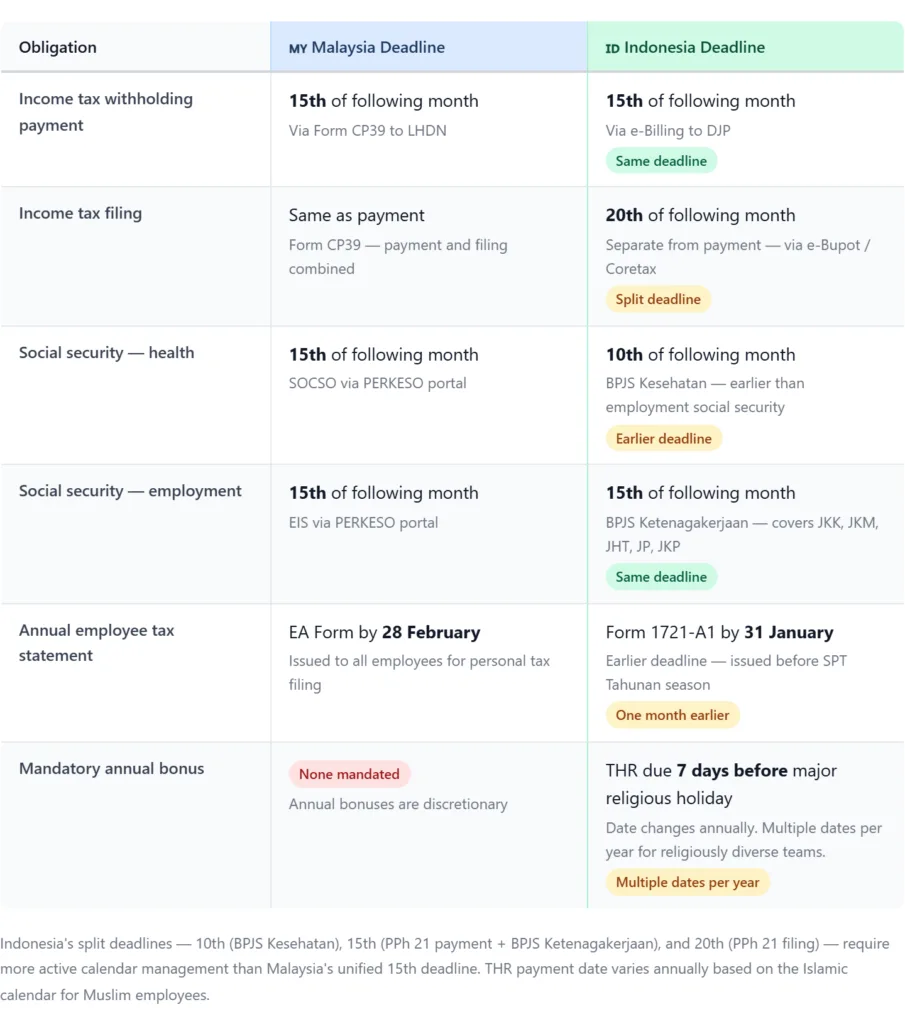

Income Tax Withholding: The PCB vs PPh 21 Gap

Both countries require employers to withhold income tax monthly. Both systems use progressive rates. Each country also imposes fixed monthly withholding deadlines. That’s where the similarities end.

The difference between Malaysia and Indonesia payroll systems becomes most visible in monthly tax withholding administration.

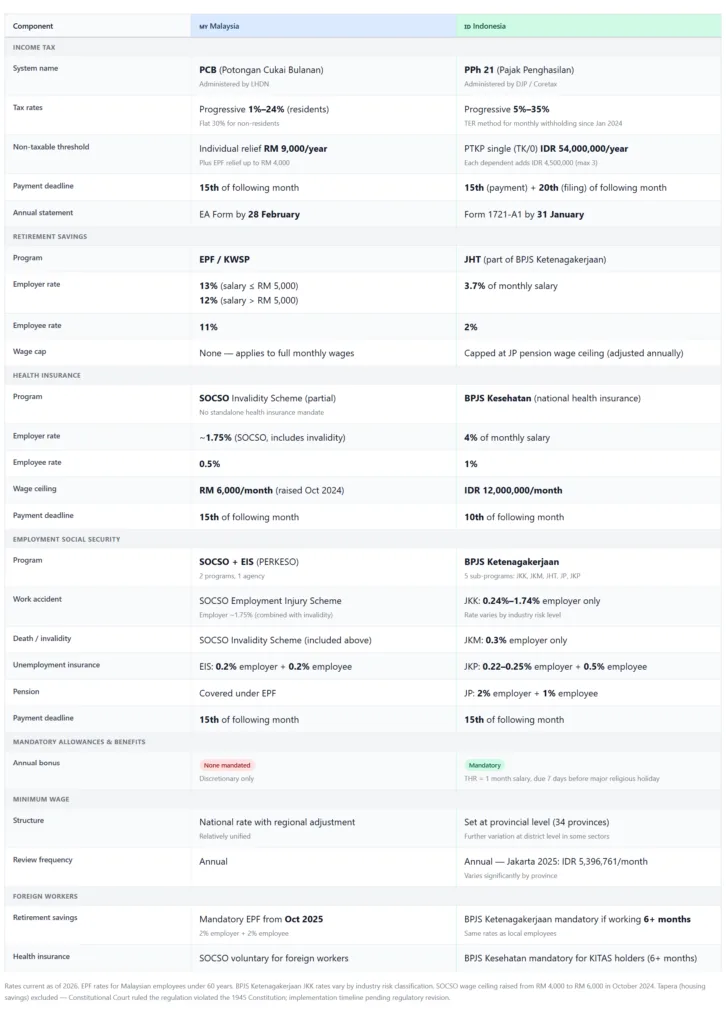

Malaysia: PCB (Potongan Cukai Bulanan)

Malaysia’s monthly tax deduction system, administered by LHDN (Lembaga Hasil Dalam Negeri), uses a progressive rate structure that currently runs from 1% to 24% for residents. Non-residents are subject to a flat 30% withholding rate on employment income.

The employer calculates PCB monthly using LHDN’s MTD (Monthly Tax Deduction) schedule or the Computerised Calculation method. It incorporates the employee’s declared personal reliefs: individual relief of RM9,000, EPF contributions up to RM4,000, spouse/child reliefs, and others. Employers must remit PCB deductions by the 15th of the following month through the CP39 submission system.

The annual EA Form summarises total remuneration, EPF contributions, SOCSO, EIS, and PCB deducted month by month. It must be provided to all employees by 28 February of the following year. This is the document employees use to complete their personal tax returns.

Indonesia: PPh 21 with the TER Method

The biggest difference between PCB and PPh 21 lies in the calculation methodology. Indonesia’s PPh 21 is governed by progressive brackets of 5% to 35%. But since January 2024, monthly withholding no longer uses the traditional annualisation method. The Directorate General of Taxes introduced a simplified Effective Rate (TER) method under PMK 168/2023, replacing the complex monthly calculation with three rate categories.

Under TER, employers apply a single predetermined effective rate based on the employee’s PTKP (non-taxable income) status and monthly gross income. It makes monthly withholding simpler, but requires December reconciliation against the standard progressive brackets.

As of 2026, BPJS rates, TER tables, and progressive tax brackets remain unchanged from the previous year. The PTKP thresholds have also not been adjusted. TK0 (single without dependents) is set at IDR 54,000,000/year, while K0 (married man without dependents) is IDR 58,500,000 per year. Each dependent adds IDR 4,500,000, up to a maximum of three dependents.

The compliance calendar is tighter than Malaysia’s. PPh 21 payment is due by the 15th of the following month, and the monthly return must be filed by the 20th through the Coretax system. Missing the 20th filing deadline, separate from the payment deadline, creates penalties that the Malaysian PCB system doesn’t have in the same form.

For multinational companies running Indonesia payroll compliance operations, the combination of the TER transition, the split payment/filing deadlines, and the December annual reconciliation creates a calculation burden that Malaysia’s PCB system does not.

Also read: Common Payroll Errors in Indonesia and How to Fix Them

Social Security: The EPF/SOCSO/EIS vs BPJS Architecture

This is the most commonly misunderstood dimension of the EPF vs BPJS comparison. Both countries have mandatory social security contributions. The structural similarity ends there.

For companies comparing the difference between Malaysia and Indonesia payroll systems, social security contributions are often where the largest compliance misunderstandings begin.

Malaysia: Three Programs, Two Bodies

Malaysia’s social security system runs through two bodies: EPF (KWSP) and PERKESO (which administers both SOCSO and EIS).

EPF employer contribution is 13% for employees earning RM5,000 and below, and 12% for those earning above RM5,000. Employee contribution is 11%. There is no contribution cap. EPF applies to total monthly wages.

Starting in October 2025, foreign workers are required to contribute 2% employer and 2% employee to EPF, a significant shift from the previous RM5.00 flat-rate employer contribution.

SOCSO provides two schemes: the Employment Injury Scheme covering work-related accidents and occupational diseases, and the Invalidity Scheme covering invalidity not related to employment. Both SOCSO and EIS contributions are subject to a monthly wage ceiling of RM6,000. The employer contributes approximately 1.75% for SOCSO; the employee contributes 0.5%.

EIS is the simplest statutory contribution. Both employer and employee contribute exactly 0.2% of monthly wages each, totalling 0.4%. EIS applies to all Malaysian employees aged 18 to 60.

All three contributions are due by the 15th of the following month.

Indonesia: Two Agencies, Five Programs

BPJS contribution rates in Indonesia cover two separate agencies with distinct contribution logic, wage caps, and payment deadlines.

BPJS Kesehatan (National Health Insurance) runs a straightforward structure: 4% employer share and 1% employee share, with the contribution cap applying at IDR 12 million monthly salary. Payment is due by the 10th of the following month.

BPJS Ketenagakerjaan covers four employment programs, each with separate rates:

- JKK (Work Accident Insurance): Employer only. Rates vary by industry risk; very low at 0.24%, low at 0.54%, medium at 0.89%, high at 1.27%, and very high at 1.74%. Most office-based roles fall under “very low” at 0.24%.

- JKM (Death Insurance): 0.3% employer only.

- JHT (Old Age Savings): 3.7% employer, 2% employee.

- JP (Pension): 2% employer, 1% employee. Subject to an annually adjusted wage cap.

BPJS Ketenagakerjaan payment is due by the 15th of the following month, five days after BPJS Kesehatan. For cross-border employers managing Indonesia payroll compliance, this split deadline between the two BPJS agencies creates a calendar that requires more active monitoring than Malaysia’s unified 15th deadline for all contributions.

The total employer burden from social security alone is generally lower in Indonesia than in Malaysia, typically 8% to 10% of salary in Indonesia versus Malaysia’s approximately 15% of salary. The mechanisms, however, are structurally different enough that one cannot simply substitute knowledge of one system for the other.

Also read: Indonesia Labor Law: Key Rules for Foreign Business

What Indonesia Requires That Malaysia Doesn’t

Two mandatory obligations exist in Indonesia’s payroll system that have no direct Malaysian equivalent, and that catch foreign companies off guard with surprising regularity.

THR (Tunjangan Hari Raya)

THR is a mandatory annual religious holiday allowance equal to one month’s salary for employees with more than one year of service. It must be paid no later than 7 days before the holiday. New employees who joined in late 2025 or early 2026 are entitled to a pro-rated THR calculated as (months of service ÷ 12) × 1 month’s salary.

For Muslim employees, THR is paid before Eid al-Fitr. For Christian employees, before Christmas. And for employees of other religions, before their respective major religious holidays. An employer managing a religiously diverse workforce in Indonesia manages multiple THR payment dates, not one.

Malaysia has no equivalent mandatory obligation. Annual bonuses exist but are discretionary. Foreign companies expanding from Malaysia to Indonesia consistently under-budget for THR because they have no mental model for a legally mandated bonus tied to religious observance.

Regional Minimum Wage Variation

Malaysia sets a national minimum wage with regional adjustments, creating a relatively manageable compliance picture. Indonesia’s minimum wage system operates at the local level: UMP at the provincial level, UMK at district (kabupaten/kota) level, and UMSP/UMSK for certain sectors.

As of 2026, Indonesia’s minimum wage system remains decentralised, with provincial and city-level rates varying significantly based on local economic conditions and labour market dynamics. Jakarta’s provincial minimum wage now exceeds IDR 5.7 million per month, while rates in Central Java and Yogyakarta remain less than half that level.

For regional HR teams trying to understand the difference between Malaysia and Indonesia payroll systems, this regional variation creates a compliance overhead that has no equivalent in Malaysia’s payroll architecture. A company operating across Jakarta, Surabaya, and Yogyakarta is effectively managing multiple minimum wage compliance frameworks at the same time.

Also read: Managing Remote Teams in Indonesia: Strategies & HR Solutions

Compliance Calendar: When Both Systems Expect Payment

The difference between Malaysia and Indonesia payroll systems becomes most practical when mapped to actual deadlines, because compliance failures in both countries are most commonly calendar failures, not calculation failures.

Malaysia’s calendar is simpler: nearly all obligations fall on the 15th, with one February annual deadline. One date to manage, consistently.

Indonesia’s calendar requires active management of four distinct dates across two tax and social security systems, plus the THR obligation whose exact date changes annually based on the Islamic calendar for Muslim employees.

For Malaysia payroll compliance teams expanding into Indonesia, this calendar shift is operationally significant. A payroll team accustomed to one recurring deadline per month will miss Indonesia’s 10th-deadline BPJS Kesehatan payment in the first months of operation unless the calendar is explicitly reconfigured.

Also read: Recruitment of Foreign Workers Regulation Indonesia: A Complete Guide

Overtime Rules: Different Limits, Different Cost Calculations

The difference between Malaysia and Indonesia payroll systems becomes especially visible in overtime administration. Both countries regulate overtime differently in terms of limits, calculation methods, and employer obligations.

Malaysia: Structured Caps with Hourly Multipliers

Malaysia’s overtime rules are governed primarily under the Employment Act 1955. Standard working hours are capped at 45 hours per week, and overtime generally cannot exceed 104 hours per month except under specific approvals or exceptional circumstances.

Overtime pay calculations follow a relatively standardised multiplier structure:

- 1.5x hourly rate for overtime on normal working days

- 2x for rest days

- 3x for public holidays

Malaysia calculates the ordinary hourly rate using the employee’s monthly salary divided by 26 working days and then divided again by normal daily working hours. In practice, the common formula is: (monthly salary ÷ 26) ÷ daily working hours.

The calculation base is therefore tied directly to the employee’s ordinary rate of pay, making payroll administration comparatively straightforward once the monthly salary is converted into hourly rates.

For payroll teams, the compliance challenge in Malaysia is usually operational: ensuring overtime hours are tracked accurately and that monthly caps are not exceeded.

Indonesia: Longer Limits, More Complex Formulas

Indonesia’s overtime framework is more calculation-heavy. Under current manpower regulations, overtime is generally limited to a maximum of 4 hours per day and 18 hours per week, excluding overtime performed on public holidays or weekly rest days.

The calculation methodology is also more complex than Malaysia’s system because Indonesia requires employers to derive overtime pay from a legally defined wage base formula:

- Hourly overtime rate = 1/173 × monthly wage

- First overtime hour: 1.5x hourly wage

- Subsequent overtime hours: 2x hourly wage

Different multiplier structures apply for overtime performed on weekly rest days and public holidays, particularly for employees working six-day versus five-day workweeks.

For regional business operators managing Indonesia payroll compliance, overtime errors commonly occur not because employers ignore the rules, but because payroll teams incorrectly apply the wage base or fail to distinguish between ordinary overtime and holiday overtime calculations.

The operational implication is significant. A company expanding from Malaysia into Indonesia cannot simply replicate its overtime policy across both countries. The legal limits, payroll formulas, and compliance exposure are materially different.

Also read: Understanding Indonesia Overtime Rate and Law

How Gadjian Handles Indonesia Payroll for Foreign Companies

Understanding the difference between Malaysia and Indonesia payroll systems is the first step. Implementing it correctly every month, across PPh 21 calculations, five BPJS programs, THR timing, regional minimum wage variation, and overtime calculations, is the operational challenge that follows.

For companies expanding into Indonesia, the payroll administration burden is significant precisely because the system is legitimate, well-enforced, and unforgiving of errors that stem from applying Malaysian payroll logic to an Indonesian compliance environment.

Cloud-based SaaS Gadjian was built for this environment, built within it rather than adapted for it.

An Automated and Compliant Payroll Process

When payroll runs at the end of the month, every statutory calculation happens automatically: gross-to-net payroll processing, BPJS Kesehatan and Ketenagakerjaan contribution calculations across all five programs, and overtime calculations using Indonesian ministerial formulas. The system doesn’t require HR teams to manually calculate each rate or formula.

PPh 21 calculation runs on the current TER method, not the pre-2024 annualisation approach that many global payroll tools still use. Monthly withholding applies the correct effective rate based on each employee’s PTKP status and gross income. December reconciliation against progressive brackets happens automatically. The Form 1721-A1 that employees need for their annual tax returns is generated from the same verified payroll data. No manual reconstruction required.

BPJS contributions are calculated correctly across both agencies, with the contribution cap applied to salaries up to IDR 12 million per month, and the JP pension wage cap adjusted as annual regulations are updated. The split between the 10th and 15th deadlines is handled within the system. HR generates the correct payment files for each agency on the correct schedule, rather than managing two separate manual processes.

A Genuine Indonesian Payroll Platform

For regional HR teams navigating Indonesian payroll for the first time or for regional teams managing both Malaysian and Indonesian operations simultaneously, this isn’t just administrative convenience. It’s the difference between a payroll operation that works and one that generates compliance gaps that compound month after month until an audit makes them visible.

The right response to that difference is not more manual effort. It’s a payroll system that was built to handle Indonesian compliance specifically, not one that was built for another market and adapted for Indonesia as an afterthought.

Web payroll Gadjian is trusted by thousands of companies across Indonesia, including foreign-operated businesses, representative offices, and regional headquarters managing Indonesian workforce compliance from outside the country.

Run payroll in Indonesia with compliance built in from day one using Gadjian, and give your HR team an automated payroll system that understands Indonesian compliance by design.